| Monthly

Article

Topics for March |

||

|

This Issue

Various Topics

Tech Talk

Market Statistics

Notice:

Copyright (c) 2002 Commodity Systems Inc. (CSI). All rights are reserved.

|

Topics discussed in this month's journal. Holiday Schedule CSI will be closed for voice communication on Friday, March 29th for the Good Friday holiday. Although U.S. exchanges will be closed, the CSI host computer will be accessible throughout the holiday weekend. Those markets that remain open will be available for updates at their normal posting times. Assessing the Economic Effects of U.S. Fiscal and Monetary Policy As an amateur student of economics, I enjoy reading and sometimes writing about economic fundamentals. Federal Reserve policies, taxation, investor sentiment and federal spending are all factors that affect our economy's future direction. I find it interesting to look for interrelationships between all of these and the balance in my own investment accounts. Although each of us is at the mercy of U.S. and other world government plans and policies, there are things we individuals can do to protect our resources. The first step, as in almost all things, is to become educated about the realities involved. For me, the key to understanding the U.S. economy is to pay attention to the policies and decisions advanced by the Federal Reserve Open Market Committee headed by Federal Reserve Chairman, Alan Greenspan. It seems to me that he has spent much of his monetary ammunition by reducing interest rates to extraordinary recent lows. This began during the precipitous market decline that occurred months before the "911" tragedy. By lowering interest rates (the discount rate and the Fed Funds rate), the government has effectively increased the supply of money. Greenspan's attempt to stimulate the economy by gradually lowering the cost of money between commercial banks did not have sufficient effect to boost our ailing economy. I don't believe Greenspan will allow the trend to continue, nor will he follow Japan's lead in lowering interest rates to the point that they approached negative territory - with sustained troubling effects. Banks represent one mechanism through which the U.S. government affects the money supply. Increases in the money supply are facilitated by commercial banks when they loan money or purchase securities. The Federal Reserve regulates the amount of money a bank can loan by imposing a "reserve requirement," which is the percentage of the bank's assets that must be on deposit at the Regional Federal Reserve Bank. For example, if a commercial bank has $1,000 on deposit in the Federal Reserve Bank and the Federal Reserve is currently imposing a reserve requirement of 10%, then the bank can grant loans totaling $1,000/.10 or $10,000. This produces a $10,000 increase in the nation's money supply. If the Federal Reserve wants to increase the money supply, it might buy U.S. Government Securities (T. Notes, for example) on the open market with a check drawn on the U.S. government. (The only cost to this transaction is the ink used to write the check because the money is created out of thin air.) When the seller of the securities deposits the government check in his commercial bank, the bank's deposits (reserves) at the commercial bank's Federal Reserve Regional Bank increase. With these increased reserves, the commercial bank can now increase the money supply (at a multiple of 10 times the amount of the government check, using the above example) by making new loans based upon the increased reserves from the seller's deposit.

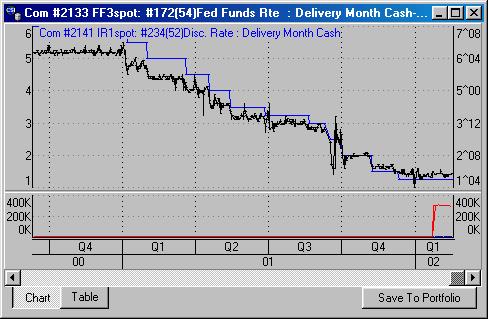

[Figure 1 Caption - The Fed Funds rate and the discount rate have simultaneously declined since January, 2001. Source: Unfair Advantage.®] Banks (not the economy) have been the greatest beneficiaries of recent interest rate cuts. The reductions in Fed Fund and Discount rates over the past year that were intended to stimulate the economy have been hoarded by banks, which did not allow the benefits to filter down to average Americans. Banks were quick to cut the interest rates they pay on CDs and savings accounts, but they have not budged on their high rates of interest for credit card balances. I'll grant you that consumers have benefited slightly from very marginal reductions in home mortgage rates and some consumer loans, but certainly not enough. It is clear that the banks kept most of the pie. The prime rate charged to businesses, on the other hand, did see a more significant drop. The effect of the interest rate cuts tended to help the auto markets, makers of household consumer appliances, and perhaps manufacturers of household furnishings. Those shorter-term interest rate cuts played a role in supporting the economy through boosts in these areas. That said, I believe lowering interest rates further than current levels, which are already quite low, will likely do little to support the economy. In hindsight, most economic professionals already claim that Greenspan was a bit too conservative by reducing interest rates on such a gradual basis. It is quite clear that a more aggressive plan should have been adopted. Lately Chairman Greenspan seems to be conflicted between activism and monetarism, a more conservative approach advocated by mid-20th century economist Milton Friedman. Friedman believed that the appropriate governmental position was to provide a steady, lightly expanding money supply. He felt that gentle control of the money supply, not government fiscal policy, should be the primary means to manage the economy. In Friedman's view, an insufficient money supply was the major contributor to the Great Depression, the economic disaster in Great Britain under Margaret Thatcher and the U.S. recession in the early 1980s. Monetarism reached its heyday in the 1970s, but soon fell into great disfavor. Today economists generally agree that pure monetarism is flawed, at best. Economic stimuli that rely on the effects of interest rates are classified as Federal Reserve-Sponsored Monetary Policy Adjustments. Because Greenspan can no longer make effective use of his interest rate control options, his arsenal of econometric power is now likely to fall into the more complex category of Fiscal Policy management. Fiscal Policy is to government spending as Monetary Policy is to controlling the cost and supply of money. Increased government spending to create jobs and legislative tax reductions are both fiscal remedies the government will likely employ in the near future. A tax cut will promote additional spending on goods and services, so our government will surely become more aggressive and engage in these fiscal alternatives. Just how this will be accomplished is a political decision. The forthcoming Fiscal Policy changes that may be required to stimulate the U.S. economy out of a recession can include federal spending for defense, roads and infrastructure improvements, airport changes, security forces and tax cuts. An objective (and possibly a byproduct) of fiscal policy incentives is the introduction of large portions of capital into the economy that will give others funds to spend or re-spend. When the economy begins to aggressively move forward again, there will be many things to watch. Fiscal Policy changes could spawn inflationary tendencies that will inevitably require raising interest rates. Should this be required, watch for auto sales to taper off as car loans and lease payments become more expensive. Such moves will spill over and constrain other categories of business such as manufacturing, tire production and other industries that supply materials to auto manufacturers. When exports become more expensive, demand will slow. Foreign economies could suffer as foreign residents exchange local currencies for dollars and gear investments to earn higher U.S. Treasury Bill interest payments guaranteed by the U.S. government. Staying abreast of economic news is fairly simple to accomplish. Unfair Advantage® (UA) customers can review important facts about the economy as they occur with a perspective that goes far into the distant past. UA's economic series on Consumer Price Indices (CPI) and Producer Price Index (PPI) changes are readily available for all to see in a graphical or tabular form. They will tell you whether prices are moving into dangerous inflationary spirals, or if they are moving in a controlled manner. Also watch the inflationary hedges like gold, silver, and oil. These commodities are great barometers of stock market despair when they jointly rise unexpectedly. When this happens, trouble may be brewing for the financial markets. Study charts covering the recent events in the gold and oil markets before taking a heavy position in the stock market. Those gold and oil traders may be hedging their bets against a possible stock market decline. UA's econometric series extend to categories of retail sales, employment and unemployment, federal budget expenditures, home sales, international trade, consumer credit, consumer confidence, the cumulative national debt, etc. These are just a few of the hundreds of series maintained and updated daily in the UA database. Watch these series to be sure your planned market positions are not in conflict with depressing economic trends, such as increasing unemployment statistics or a declining consumer confidence index. UA, which provides data on markets traded in every major financial center on earth, gives you the necessary tools to inductively determine the future course of major financial markets. When the markets react, sometimes violently, to seemingly subtle bad news, look a bit further into UA's data archives. You may quickly learn what prompted the reaction, and realize that future reactions might be predictable as well. The Fed has

a difficult job in controlling the forces that make the economy work, but with

your data-banking laboratory in the form of UA, you can more easily understand

these forces. Use Unfair Advantage to educate yourself, and use that knowledge

to navigate a safe course for your investments.

Bob Pelletier More on Spread Strategies In last month's CSI Technical Journal, we wrote about UA's Online Newspaper feature and ways to benefit from studying its correlation tables and graphic displays. The tables provide data on the most positively and negatively correlated markets, and are likely to reveal several opportunities for profit using spread trades. The graphics show the normal price movement for pairs of markets and indicate the degree of variance from their normal relationship. Spread and straddle trades can often be profitable when the investor looks for and acts upon variances from the normal relationship between highly correlated pairs. For example, if Crude Oil and Gas Oil normally move in tandem, but suddenly the prices for the pair take divergent paths, it is quite likely that one or both will soon make a change, resulting in two markets that again move in tandem. The trick for the investor is to profit from the two markets' natural tendency to return to their normal relationship, be it as highly positively or highly negatively correlated pairs. As mentioned last month, in a diverging positively correlated pair, the trader should be prepared to sell the stronger market and buy the weaker one. Conversely, when a negatively correlated pair moves together, your job is to take positions that will capitalize upon their tendency to move apart. One important aspect to remember about spread and straddle trades is that the dollar value of both legs should be roughly equal. For example, if the value of the commodity you are shorting is $30,000 per contract and the value of the desired long position is $10,000 per contract, you should triple up on the long position to make both legs balance at $30,000 each. Balancing your investments can be more complicated than this, but it is a worthwhile exercise that can usually be accommodated by either adding contracts or selecting compatible contract sizes from various exchanges.

Unfair Advantage allows you to view the full contract value of your commodities through a feature on the charting "Right Click" menu. See the above chart for an example. Note that both scales show U.S. dollars per contract, as opposed to dollars per ounce or 32nds, as would normally be presented.

|