[Click here to return to journal index]

June 2006

CSI Technical Journal

Volume XXIV, Number 6

In This Issue

Holiday Schedule

CSI will be closed for voice communication on Tuesday, July 4th in observance of the U.S. Independence Day holiday. All U.S. exchanges will be closed. Data from other markets will be available at the normal posting times, and the CSI host computer will be accessible as usual.

Trading Negatively Correlated Markets to Achieve Positive Profits

"I'm a great believer in luck, and I find the harder I work, the more I have of it." -- Thomas Jefferson

There are traders who believe that luck plays an important role in their financial success. I am, as Thomas Jefferson was, more inclined to believe that a good result good luck, if you will, comes from hard work. In fact, I sign on to the motto, the harder I work, the luckier I get. What kind of work makes a successful trader? Reading, analysis and trial-and-error experimentation.

For instance, if you were to take the time to study the mathematics behind Nobel Prize winner Harry Markowitzs contribution to Modern Portfolio Theory,1,2 you would learn how useful it is to explore the relationships between markets within your trading portfolio. Correlation avoidance was Markowitzs theme, and one that we have explored in recent CSI Technical Journal articles. Regular readers will recall techniques for avoiding risk by removing positively correlated markets from your portfolio.

Want to get luckier? Read on for more information about exploring both ends of the correlation spectrum, that is, both positive and negative correlations. Although last months CTJ touched on the benefits of trading negatively correlated markets, I will discuss this strategy in more depth here, so that you can readily see how one might profit from it. This is a powerful approach to trading because with it, market risk may be controlled.

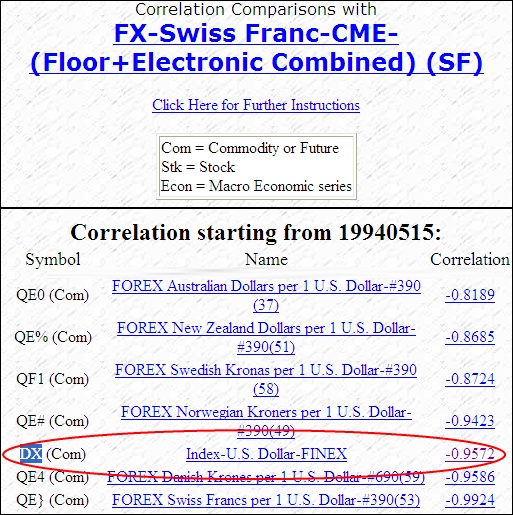

To achieve profits trading negatively correlated markets, your initial focus must be on finding related markets that have inverse pricing patterns. The first step is to identify a starting market that will make up one half of a market pair. For illustrative purposes, suppose we choose the Swiss Franc market. We can introduce Swiss Franc by entering its symbol, SF, into the CSI website Correlation Study. (Get there through Unfair Advantages® Trading Tools menu). For this example, I did a 12-year study on futures only, and analyzed Swiss Franc against all other futures traded worldwide.

To profit from diverse market relationships such as are exhibited through a highly negative correlation coefficient, one should first look at the bottom of the correlation table (see example above) to find strong negative values. Remember that a total lack of correlation is reflected by a correlation coefficient of zero (0.0), so anything beyond -0.6 is fairly strong and beyond -0.7 is stronger still.

The bottom of the Correlation table lets us see which markets have the highest negative correlation values. A review of our example reveals that DX, the U.S. Dollar Index, has a negative correlation coefficient of minus 0.95 with the Swiss Franc. This is a very strong negative correlation for the market pair. It means that when the Swiss Franc increases in price, the dollar index tends to fall in value; when the Swiss Franc decreases in price, the dollar index tends to rise. The relationship is understandable because the Swiss Franc contract is measured against the U.S. Dollar.

The phenomenon of having a strong inverse relationship does not necessarily describe a condition where movement in a particular market triggers the other to move in the opposite direction. It could represent both markets responding in opposite ways to the same stimuli in the economy. For example, some agricultural commodities tend to show negative correlations with blue chip stocks: Wheat and General Electric -0.698; IBM and Cotton -0.754; .Whatever the relationship, be it cause-and-effect or divergent responses to economic conditions, a strongly negative correlation coefficient is a suggestion that these markets will move against each other a specified percentage of the time. And, of course, the closer the coefficient of correlation approaches unity (1.0 or -1.0), the better will be the consistency of the result. In rare instances, what appears to be a strong correlation is merely an extreme coincidence.

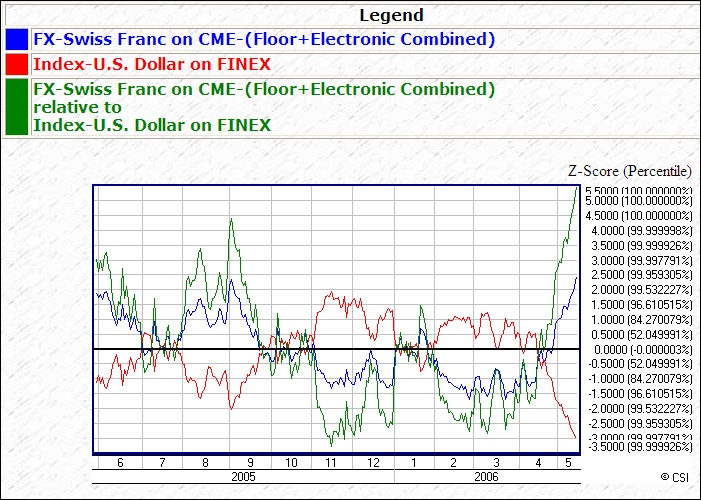

While it is clear that the Dollar Index and Swiss Franc are related markets and that their pricing pattern is inverse, these characteristics are not enough to indicate a trading opportunity. You should also look for markets that have oscillating Z-scores over time. Z-scores are found by clicking the correlation coefficient for your chosen pair, which is at the right in the Correlation Studies table. The seemingly consistent relationship between the Swiss Franc and the Dollar Index is shown in the example below.

Please notice the charts scale. Z-scores generally fall between the statistical levels of +3 and -3. This quantity is a measure of the number of standard deviations or sigmas that prices are separated over time. A statistical level of +3 or 3 standard deviations accounts for perhaps 99% of the markets price difference. It is unusual to find levels that are outside of the + or 3 range, but we have seen the range expand beyond that level for some of the market pairs we studied.

Market Timing

When a negatively correlated pair with divergent, oscillating Z-Scores is found, the opportunity for low-risk profits involves selling (shorting) the market that is statistically higher and buying (going long) an equivalent dollar lot of the market that is statistically lower. This straddle trade is made in anticipation of a closing of the gap between the negatively correlated market pair. When one goes up, the other comes down, and vice-versa. It is recommended that you use the Correlation Study and Z-score chart to determine which markets to trade in which direction, and additional technical trade-timing programs to time specific market entry and exit points.

One should only enter a straddle trade when one market clearly exists at the upper market extreme, and its counterpart exists at the lower market extreme. When the pair of markets oscillate (as their z-scores cross and reach the opposite extremes), one should offset the positions by executing simultaneous sell and buy orders. Ideally, a level of -2 or -3 may match up nicely from a positive Z-score start, but such an extreme reaction may not always materialize. However there will be a natural tendency for the pair of markets to cross over each other to complete a cycle. One can generally see opportunities when markets oscillate nicely, but be very cautious not to expect too much out of such behavior. Just know that the Z-score differences will tend to behave in a more or less predictable manner, making occasional opportunities for profit as the markets attempt to return to expected norms near the center of the overall range.

A persistent inverse relationship is demonstrated through Perpetual Contract® data for the Dollar Index and Swiss Franc.

Matching Investments

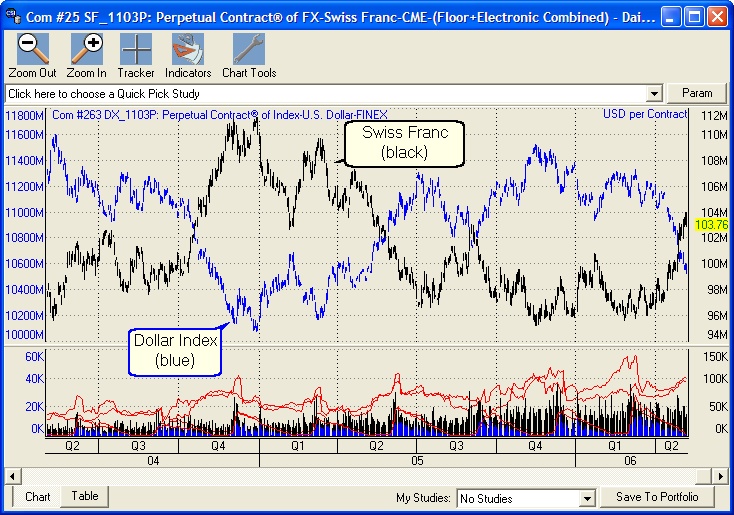

Matching up your capital investment for each of the respective markets is an important part of the operation. Commodity contracts come in different sizes and lot quantities, so you will likely find yourself in a situation where the dollar value of one contract of commodity A is not balanced with the value of one contract of commodity B. The goal should be to balance investment risk of the market pair, so as not to over-invest in one at the expense of the other. To help make this easier, UA will allow you to chart the markets as either price-per-unit or price-per-contract. The chart above shows full contract values for both the Dollar Index and Swiss Franc, allowing you to see that they are valued differently.

Similarly, an ounce of gold will not match up with a pound of live cattle, but the full value of two cattle contracts at $34,000 each balances roughly with a the $68,000 value of a single gold contract (or it would have before Gold raced above $700 an ounce last week). Naturally, your investment wont be so large in your margined account, but the investment risk should be based on the ratio. Knowing the value of your contracts should be helpful in balancing risk. Allow the correlation coefficient to guide you in matching up pairs based on market directional influences. Then use your knowledge of those markets to trade off similar dollars of product for each leg of the dual-market straddle.

Some other interesting negative correlation opportunities involving commodities include: Feeder Cattle vs. Feed Wheat, Cocoa vs. NASDAQ 100 Index, Coffee vs. U.S. Treasury Notes, British Pound vs. the Dollar Index, the Canadian Dollar vs. the Dollar Index, Gold vs. the Dollar Index and the S&P 500 vs. Treasury Bonds.

You could run a correlation study that looks for correlations between the universe of futures and the universe of stocks. These studies abound with interesting relationships. An example would be the fairly strong inverse relationship of -0.62 between Natuzzi, whose furniture collections are known for their fine leather upholstery, and Live Cattle.

There are many other pairs of negatively correlated markets that represent balanced risk opportunities. Seek them out through the Correlation Studies (a premium CSI service). For additional insight, it may also be helpful to expand the period of view beyond a nominal 12-year period. Look over the many opportunities, and you just might find that you are starting to log more profits in your account with less risk.

A Challenge for our Readers

Tokyo Rubber (symbol JRU), and Comex Gold (GC) appear to be correlated at the 92% level over a 12 year period. Is this one of those rare coincidences where unrelated markets appear to be correlated, or is there some connection here that were missing? If you have any insight on what makes these markets so highly correlated, please let us know.

Now that weve established what makes a trader lucky, I hope that youll use the resources at hand to improve your own fortunes. That means, of course, work hard: Read what the experts have to say and explore new techniques analysts are using. Then find out what works for you. I hope that you are finding this newsletter helpful in your day-to-day trading pursuits. If we can help you to understand a particular aspect of our service, please let us know how. We want to help you become a better trader.

Happy Trading,

Bob Pelletier

(1) Markowitz, H. (Harry), 1927 Library of Congress. Portfolio Selection: Efficient Diversification of Investment.

(2) Markowitz, H. M., 1987, Mean-Variance Analysis in Portfolio Choice and Capital Markets. New York: Basil Blackwell.

What is a Z-Score?

In statistical analysis, a Z-score is the statistical significance of today's price relative to the recent past, as reflected in signed units of standard deviation. Standard deviations of three or four identify an extreme event that is sufficiently unusual that it may occur only 1 to 5 times over the past 100 days. We believe that one should pay particular attention to such market events because significant market movement is often preceded by extreme Z-score readings.

Larger CSI numbers are coming!

Open the specifications file (longer_csinumbers.doc) and the sample data file (20060517.CSE) under UA Specifications.

Speed Enhancement

Faster downloads and distributions may be in your future with Unfair Advantage. We recently announced an upgrade that would streamline updates, making it possible for many customers to capture daily updates in a small fraction of the time currently required. The release was delayed, but this new version of UA should be available by the time you read this or shortly thereafter. Please check our website for availability or call Marketing or Technical Support for information.

Sierra Hotel

As we write this newsletter, we can report that our version of Sierra Hotel has made it possible for CSI to log unrealized profits of $3,800 in a $10,000 proving account from our one-contract short trade in the Dollar Index. This testing account represents the only active account that CSI has ever ventured to trade, so there are no hidden losses to offset the as-yet unrealized profits. Well keep you posted on our progress.

We are taking orders for the Sierra Hotel trading system, should any customer wish to give it a try. We are offering a 30-day money-back guarantee subject to our explicit Conditions of Use memorandum. Please visit our website for full details and contact our market representatives if you have any questions or wish to place an order. Past performance is no guarantee of future success.

1.800.274.4727

1.561.392-8663

Tech Talk

Tech Talk is a monthly column where the CSI Technical Support staff addresses topics of interest to many CSI subscribers. This month they will discuss the best update time for VantagePoint users, the detrending method used by CSI, data compilation and CSIs position as a software vendor.

Q. I just started using VantagePoint with CSIs EzDownloader. Today I noticed that my download was incomplete. Im missing prices for several commodities. How can I avoid this?

A. You probably requested your data before everything in your portfolio had been updated. To assure a complete download, VantagePoint customers should always call for data after 6:30 p.m. eastern time. Anyone using UAs standard downloader can be virtually guaranteed a complete update by using the Wait for

option on the Download/Distribution screen. Select your latest-reporting exchange, and UA will automatically download data as soon as that exchanges report has been posted. By the way, any time you miss data due to an early update or a late posting, UA will automatically pick up those missed prices on your next retrieval session.

Q. What method is used for detrending CSI data?

A. It is a linear process where the furthest distant closing price is linearly forced to be set equivalent to the final (most recent) closing price on file. All points in between are moved proportionally to their time-distance from the last price on file. To accomplish this, we simply look at the first closing price on file and the last closing price on file and adjust all points in between, forcing the trend to flatten the entire time series presented. The very last closing price will remain as quoted, but all earlier prices will be moved up or down respectively so that the very first closing price will be equal to the final closing price.

Q. My ticker service compiles highs and lows for the day, but the daily ranges it calculates for Chicago Mercantile Exchange (CME) markets do not match those quoted by CSI. Why not?

A. The CME counts bids that are higher than the highest actual trade and asks that are lower than the lowest actual trade as part of its official time-and-sales figures. Their logic behind this is that these bids and asks represent unrealized buying or selling pressure. CSI and most data services report these official, exchange-sanctioned figures, but they would not show up in a compiled record of actual trades.

Q. I see that CSI is now selling a propriety trading system that generates market signals. Has CSI become a registered Commodity Trading Advisor?

A. No. Although the program we are offering, Sierra Hotel by Mesa Software, does generate trading signals, those trade recommendations are not tailored to any particular trader and are not based on any traders personal situation. To quote from the rules, we are exempt from registration because CSI does not engage in any of the following activities: Directing client accounts; or Providing commodity trading advice based on, or tailored to, the commodity interest or cash market positions or other circumstances or characteristics of particular clients. Please respect our position and do not ask our staff to direct you in your trading activities. They are neither trained nor licensed for that activity. To comply with C.F.T.C. rules, CSI is prohibited from commenting on trading situations.

Notice:

The views and information expressed in this document reflect the opinions and experience of the author Robert C. Pelletier. Neither CSI nor the author undertake or intend to provide tax advice or trading advice in any market or endorse any outside individual or firm. All recommendations are provided for their informational value only. Readers should consult competent financial advisors or outside counsel before making any software purchase or investment decision. CSI does not stand behind or endorse the products of any outside firms.

Website Links: This CSI website and Unfair Advantage system contain hyperlinks and automatic links to websites operated by parties other than CSI. No association with or endorsement of third-party websites should be inferred through these links. They are provided for your convenience and reference only. CSI is not responsible for and has no control over the content of third-party websites.

All information and data on this website are © Copyright 2002-2005 by Commodity Systems Inc.(CSI) All rights are reserved.

800-274-4727 | 561-392-8663 | 561-392-1379 (Fax)