[Click here to return to journal index]

© Copyright 2003-2004 by Commodity Systems Inc. (CSI). All rights are reserved.

Website Links: This CSI website and Unfair Advantage system contain hyperlinks and automatic links to websites operated by parties other than CSI. No association with or endorsement of third-party websites should be inferred through these links. They are provided for your convenience and reference only. CSI is not responsible for and has no control over the content of third-party websites.

The CSI Team - At your service:

Andy, Betty, Bob, Debbie, Denise, Fran, Heather, Jason, Jeanean, Jose, Josh, Kathy, Ken, Kurt, Linda, Mike, Nassrin, Patti, Ron, Rosie, Rudi, Sabrina, Sean, Steven and Terry.

|

May 2004

CSI Technical Journal Volume XXII, Number 5 |

Page 1 |

Topics discussed in this month's journal:

Holiday Schedule

CSI will be closed for voice communication on Monday, May 31st for the Memorial Day holiday. U.S. exchanges will be closed, but data from other exchanges will be available at the normal posting times. The CSI host computer will be accessible throughout the holiday weekend.

Seeking Wisdom In Intermarket Correlation Reports

It is said that the question of a wise man is half the answer.* This is most certainly true in the field of market analysis, particularly when the question involves intermarket trading. It isn't enough to ask the likely direction or value of a thing, as the result will be much more valid if it also relates to the direction or value of other related things. The mathematical relationship between markets (their correlation coefficient) reflects the degree to which markets have similar responses to common economic conditions. Therefore, there is greater wisdom in asking a multifaceted question involving the future direction of multiple related markets than in inquiring about a single market.

But where does this wisdom begin? How can traders know which markets are related and which are not? The CSI website now offers correlation tables that pair all major stock and futures markets. This includes over 800 futures markets and over 15,000 stocks, making it an enormous repository of information. What this means to our customers is that you now have great insight into which markets are statistically related. All commodities are paired, all major stocks are paired, and your choice of commodities and major stocks can be paired, revealing a positive or negative correlation coefficient identifying the level of correlation for each pair. This information leaves you poised to the ask questions that bring meaningful answers.

As a trader, you should know that when items are strongly correlated in a positive or negative manner, those markets can be paired off against each other to take advantage of opportunities that aren't necessarily obvious. You can either simultaneously buy the discounted item and sell the other or simply trade one item, with the expectation that it is likely to move in the opposite direction of the other. There is much that can be done to profit from knowing the substance of the statistical relationship between markets.

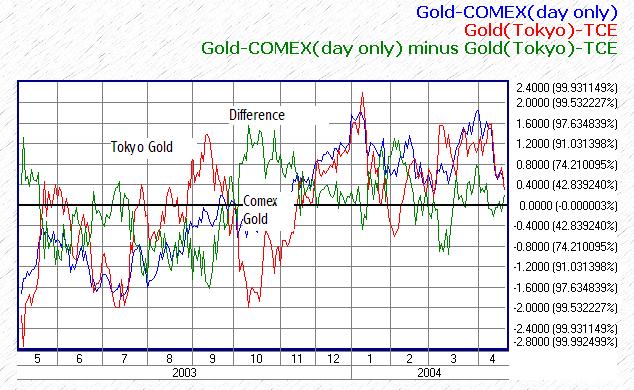

If you were to pair off COMEX Gold from the U.S., which is priced in dollars with Gold from the Tokyo Commodity Exchange in Japan, which is priced in Yen, the arbitrage differential would be quite distorted if raw prices were used for evaluation. However, if you apply the exchange rate of one with the other by converting to a common denominator of either Dollars or Yen, the correlation becomes quite remarkable.

On our website studies, when the units of trading differ or the conversion factors differ between any pair of markets, we normalize one market to be priced in equivalent units to the other. The pairing takes into account a common currency so that we have in a sense, a common denominator allowing you to accurately compare markets that are traded in different countries.

Simulated Comex gold and Tokyo gold correlation chart before conversion to a common currency. Here the correlation coefficient is .674.

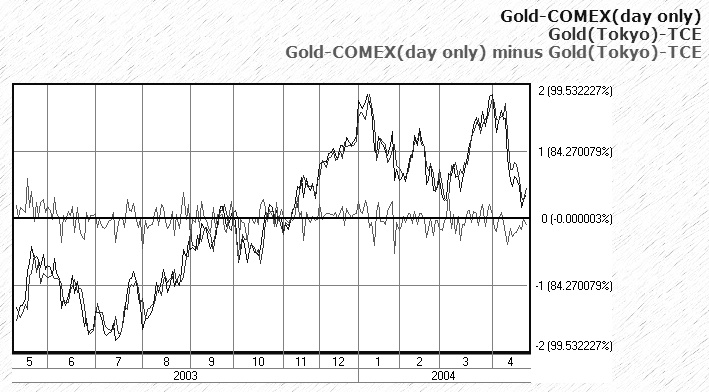

Please consider the upper chart at left. It pairs dollars off against Yen for the same gold metal. When you convert Tokyo Gold traded in Yen to Tokyo Gold traded in dollars (lower chart) the pair of markets fall together closely in almost lockstep, leaving an abundantly clear picture that there is little chance for profiting from such a seemingly profitable arbitrage opportunity. Note the relatively small differences between these markets.

When the Yen denominator for Tokyo gold is changed to dollars, the correlation moves toward perfection (1.0).

Other differences are also evident for similar products that are not so well behaved as the international gold market. But in those cases, there may be an opportunity for trading off one with the other.

Consider the highly correlated Live Cattle and Feeder Cattle markets. If the Live Cattle waveform is highly correlated with a Feeder Cattle chart and the Live Cattle side of the equation is rising in price as the Feeder Cattle falls, the possibility of profiting from simultaneously selling the overpriced item and buying the underpriced item may exist. Since correlated markets tend to move together, there may be an excellent opportunity to profit from the difference in the spread when those markets return to a more normal relationship. In such an application, the pricing of the two different correlated products need not be comparable in terms of price per pound or price per ounce etc. to make the scenario work to your benefit. You are simply betting that each member of the correlated pair will reverse their respective directional movement, returning to the normal situation where they move together. You can view this relationship yourself on the CSI website.

If you are contemplating trading a given stock or futures market, you should go to CSI's website and click "Enter Here" from the banner at the top of the page for the Online Newspaper. Click the "Correlation" button at the lower left of the Newspaper screen to have your choice of viewing correlations for commodities, stocks or both. Depending upon your browser configuration, you may need to enter your CSI User ID (in all CAPS) and customer number to access the correlation area, which is available only to customers.

This screen gives you the choice of viewing a Market Correlation report for "Futures Only," "Major Stocks Only" or "Futures and Major Stocks." Click on your choice for the desired time period, selecting from 12 years, 20 years, 30 years or 40 years. A table displays showing the markets with the highest correlation and those that are least correlated over the selected time period. You may scroll through the lists to look for trading opportunities, or you may enter a single market or any two markets (futures, stocks or one of each) into the boxes above the table.

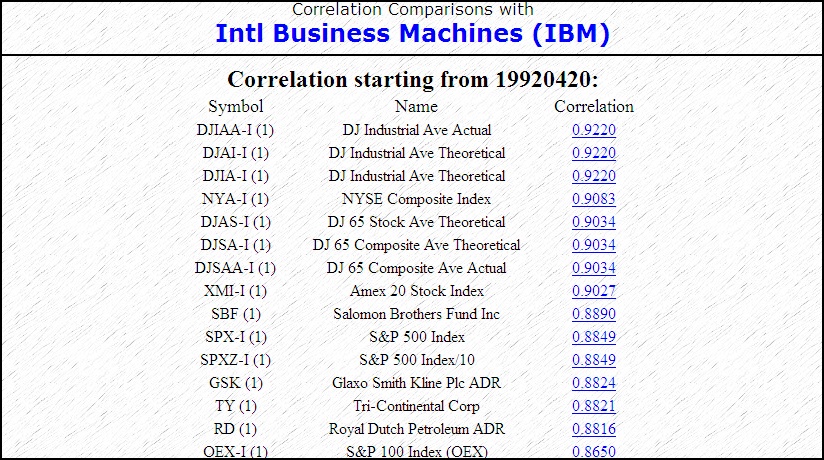

If you would like to view correlation reports for a single market, enter its symbol and then select "Stock" or "Commodity" from the drop-down menu. Next click "View Correlation Table." The CSI website will display a list of highly correlated major stocks as they compare with your chosen market. For example, IBM (International Business Machines) presents itself as a bellwether for the broader market through its high correlation to the Dow Jones Industrial Average, the NYSE Composite and a host of other stock indices. You could find other crowd-leading stocks by requesting the Dow Jones Industrial Average itself (symbol DJIAA-I) and, perhaps more interestingly, find those that consistently buck the trend by scanning the least correlated markets at the bottom of the list.

From the CSI websites Correlation tables -- IBM (International Business Machines) presents itself as a bellwether for the broader market through its high correlation to the Dow Jones Industrial Average, the NYSE Composite and a host of other stock indices.

If you have a particular pair of markets in mind that you want to test for positive or negative correlation, enter their symbols in the paired boxes labeled "Symbol 1" and "Symbol 2." Be sure to identify each as either a commodity or stock and then click the button to request the report. This will produce a graphic display based on daily pricing statistics on the two markets (converted to U.S. dollars, if necessary). The chart shows the two series and a graph of their difference like the gold charts on page 2. The price series are each scaled by subtracting the whole-chart mean and dividing by the whole-chart standard deviation to get their Z-scores, which are presented graphically. The difference of these Z-scores is also shown. The scale on the right includes both Z-score and the implied normal probability.

As you find markets that have a very high (positive) correlation or very low (negative) correlation coefficient, you might consider taking a position whereby you will benefit from a return to their normal relationship. Or taking opposing positions in a pair of markets that are heavily correlated as a hedge against further opposing movement.

These correlation studies have been invaluable in our market study work here at CSI. They show us which questions to ask in developing studies and which markets to watch for predictable movement. They offer similar benefits to all users. The correlation studies are free through the website to CSI daily update subscribers using Unfair Advantage®, and are available to others for a small monthly fee. Not a bad price for the beginning of wisdom!

Prior CSI newsletters have hinted at a trading approach that would revitalize CSI's plans to expand upon the popular Probable Direction Index (PDI) that was included in CSI's QuickTrieve® data collection system in the 1980s. PDI was publicly announced in Stocks and Commodities Magazine in an interview article, which led to a TV interview on FNN (now known as CNNfN) with John Bollinger. PDI is being revisited in a comprehensive manner that introduces further intelligence like the ideas introduced above, and many other factors known to contribute substantively.

Our plans to move forward with a new PDI-like study are still under development. The goal is to produce a tool that will be a great help to investors. All trading will be tracked in the forthcoming version and the user will be advised to buy, sell, reverse or hold all positions as account equity varies over time. We have introduced other support tools that will allow the user to follow the markets with stops, etc. and introduced algorithms that are designed to make the decision-making effort explicit and reliable.

Happy Trading,

Bob Pelletier

* Attributed to Solomon IBN Gabirol (A.D. 1021 - 1089)

Tech Talk

Each month in this column, the CSI Technical Support Staff addresses topics of interest to many subscribers in a question-and-answer format. This month they discuss CSI's proportionally back-adjusted data series, CSI's Data Release Schedule and discrepancies in stock price data between vendors.

Q. Do CSI's proportionally back-adjusted series give an accurate percent return?

A. Yes, they do. We have always known this, but are pleased to report that a customer recently calculated values by hand to test our automated figures. He wrote us the following: "I'm glad to determine that the proportional method gives the correct percent gain/loss. I am now at ease, confident that CSI's data is correct." We appreciate the positive feedback.

Q. Please give an example of how adding a fixed number to back- and forward-adjusted continuous contracts affects prices. I'm particularly concerned with rounding and the avoidance of negative numbers.

A. We have recently revised our manual as follows, so the description is now supplemented with an example. "Back- and forward-adjusted continuous contracts can regress to negative values into the past. This [Add a Fixed Amount to Make Non-Negative] is one of two options allowing you to avoid negative numbers. The resulting data (including current contract prices) will be adjusted upward by the absolute value of the maximum dip below zero rounded up to the nearest 1,000 points. For example, if a PB series gets down to -69.07, then 6907 is rounded up to 7000. The low price of the modified series is then -69.075 + 70.00 = 0.925 which would display as .92." We hope this clarifies the procedure.

Q. Some of the stock prices I get from CSI are different from those quoted by other vendors. Why is that?

A. CSI stock data is a composite of all regional exchanges, including the late-closing Pacific exchanges. If our data is compared with the early-closing NYSE, there will undoubtedly be differences, especially in highs and lows. This is because trading ranges can expand after the NYSE closing bell.

Our values may also be different from those provided by some vendors because of a difference in the handling of dividends. CSI's algorithm proportionately adjusts the data based on the price the day before x-dividend day, whereas some services use the price on the day of the dividend. We have investigated the procedure and find no consensus on which approach is more correct. Both are commonly done. Therefore, the technique for applying the proportional adjustment is a matter of style or convention, and the results of either calculation should be considered correct.

You are right that CSI stock data may be different from other vendors', but from a complete scope perspective, we believe CSI's stock series are about as good as is humanly possible.

Q. My CSI stock data was late one day this month. Is this likely to happen again?

A. Not if we can help it. That late posting occurred when we made some changes to our system, and as a result, we have modified our practices to avoid a repeat. In general, our postings have been ahead of schedule. Here's a sample of our internal posting reports:

| # | Target | Actual | Name |

|---|---|---|---|

| 1 | 10:45 am | 10:25 am | Pacific Rim Commodities Released |

| 2 | 4:00 pm | 3:41 pm | European Commodities and LSE Released |

| 3 | 5:10 pm | 4:24 pm | Preliminary Stock Copy |

| 4 | 5:45 pm | 6:19 pm | Early North American Futures Released |

| 5 | 6:30 pm | 6:22 pm | Montreal is Released |

| 6 | 6:45 pm | Omitted | CBOT and CME Released* |

| 7 | 7:30 pm | 7:12 pm | The Official Stocks, Mutual Funds, and most Indices Released |

| 8 | 7:45 pm | 7:25 pm | Cash Series for Above Markets and All Remaining Data Released |

| 9 | 8:15 pm | 8:00 pm | After Newspaper Copy |

| *This posting was combined with the "Early" data release at 6:19. | |||

800-274-4727 | 561-392-8663 | 561-392-1379 (Fax)