Effective July 10th, 2017, CSI will resume coverage of E-mini Russell 2000 Index futures and options on CME under CSI#677 (Symbol ER2). The existing contracts on ICE will continue to be available under CSI#818 until expiration. For more information, see the CME News Release

CANADA DOLLAR MINIMUM TICK CHANGE — 2016 JULY 8

Effective Sunday, July 10, 2016 for trade date Monday, July 11, 2016 the Chicago Mercantile Exchange will amend the minimum price increment for Canadian Dollar Futures. The minimum tick is changing from 0.0001 to 0.00005.

Users of UA versions before 2.10.8 will need to refresh the database history for the affected data sets.

Click here for instructions.

CSI issues affected:

#64 CD

#129 CD2

#880 CD1

#100819 MCD

Taiwan Futures Exchange market closed 2016 July 8

Taiwan Futures Exchange announces that the market will be closed on 2016/7/8 due to Typhoon Nepartak. The Final Settlement Day of the 201607 TOPIX Futures contract will be postponed to the next trading day accordingly. The final settlement price of the contract is the TOPIX Special Quotation (TOPIX SQ) calculated on the final settlement price determination day (the TSE business day following the last trading day, 2016/7/8).

This effects the following CSI#s

#644

#645

#646

#448

#751

#100161

#650

#100489

#100492

#100493

FX PRECISION CHANGE — 2016 MAY 2

Effective Monday, May 2, 2016 certain cross-rate quotes will gain an additional digit of precision.

UA users will need to refresh the database history for the affected data sets.

Click here for instructions.

CSI issues affected:

| CSI# | Delivery Code | Old decimals | New Decimals | Cross | UA Symbol | UA Number |

| 171 | 37 | 4 | 5 | AUD-GBP | AD3 | 2160 |

| 171 | 39 | 2 | 3 | AUD-JPY | AD4 | 2162 |

| 390 | 41 | 3 | 4 | USD-DKK | QE4 | 2254 |

| 390 | 56 | 3 | 4 | USD-MXP | QF5 | 2269 |

| 390 | 58 | 3 | 4 | USD-SEK | QF1 | 2271 |

| 390 | 60 | 1 | 2 | USD-KRW | QF3 | 2273 |

| 590 | 41 | 3 | 4 | GBP-DKK | DR4 | 2314 |

| 590 | 44 | 3 | 4 | GBP-HKD | DR7 | 2317 |

| 590 | 46 | 2 | 3 | GBP-JPY | DR9 | 2319 |

| 590 | 56 | 3 | 4 | GBP-MXP | DR8 | 2329 |

| 590 | 57 | 3 | 4 | GBP-ZAR | DR0 | 2330 |

| 590 | 58 | 3 | 4 | GBP-SEK | DR6 | 2331 |

| 591 | 46 | 2 | 3 | EUR-JPY | EU5 | 2345 |

| 591 | 55 | 4 | 5 | EUR-GBP | EU7 | 2347 |

| 690 | 38 | 4 | 5 | USD-BHD | US4 | 3301 |

| 690 | 41 | 3 | 4 | USD-CZK | US7 | 3304 |

| 690 | 45 | 2 | 4 | USD-INR | USA | 3308 |

| 690 | 46 | 4 | 5 | USD-KWD | USB | 3309 |

| 690 | 49 | 3 | 4 | USD-RUB | USE | 3312 |

| 690 | 58 | 3 | 4 | USD-PEN | USN | 3321 |

| 691 | 44 | 0 | 2 | EUR-IDR | EUH | 3331 |

| 691 | 45 | 2 | 4 | EUR-INR | EUI | 3332 |

| 691 | 49 | 3 | 4 | EUR-RUB | EUM | 3336 |

| 691 | 52 | 3 | 4 | EUR-THD | EUP | 3339 |

| 691 | 53 | 3 | 4 | EUR-TWD | EUQ | 3340 |

| 775 | 57 | 2 | 4 | ZAR-JPY | JPYXI | 3521 |

| 776 | 43 | 2 | 3 | CHF-HUF | CHFX4 | 3529 |

| 776 | 53 | 3 | 4 | CHF-THB | CHFXE | 3539 |

You can paste the list below into your refresh history dialog:

2160

2162

2254

2269

2271

2273

2314

2317

2319

2329

2330

2331

2345

2347

3301

3304

3308

3309

3312

3321

3331

3332

3336

3339

3340

3521

3529

3539

Futures Symbol Changes

In an effort to maintain consistency among CSI platforms, the following futures markets have changed symbols as of April 12, 2016. Please adjust your software accordingly. If you must use the old symbol, it is possible to modify the symbols in your UA factsheet. Contact CSI customer support if you need assistance.

| Csinum | IsActive? | Old Symbol | New Symbol | Name |

|---|---|---|---|---|

| 55 | N | LW | LWS | Sugar #4-CASH-(LCE)-EURONEXT |

| 81 | N | PE | PE9 | Euro Bond-(MATIF)-EURONEXT |

| 85 | N | RD | RD? | Deutsche Mark Spot Rolling-CME |

| 109 | N | UD | YE | mini Eurodollar(3Mth)-CBT(MACE) |

| 118 | N | HA | HAU | Gold-Hong Kong-(HKFE)-HKEX |

| 122 | N | SA | SAU | Gold-(SIMEX)-SGX |

| 155 | N | YL | YLC | Cattle-Live-SFE |

| 163 | N | ZD | PZD | Deutsche Mark-PBOT |

| 164 | N | ZE | PZE | EuroCurrUnit-PBOT |

| 175 | N | FS | FSE | Eurodollar(3Mth)-EURONEXT(LIFFE) |

| 225 | Y | YT2 | YT1 | 10-Year Australian Govt Bond (6%)-(rounded #381)-SFE |

| 256 | N | SJ | SJ9 | Japanese Yen-SGX(SIMEX) |

| 267 | N | JF | JFY | Euroyen-1 Yr-TFOREX-(TIFFE) |

| 273 | N | AP | APT | Potatoes-EOE |

| 286 | N | LA | LAM | Lambs-EURONEXT(LCE) |

| 313 | N | JC | JCT | Cotton-TCE |

| 325 | N | KP | KPK | Palm Kernel Oil-MDEX |

| 334 | N | FM? | MF? | French Medium Govt Bond(3/5Yr)-(MATIF)-EURONEXT |

| 335 | N | PO | POM | Potatoes-EURONEXT(MATIF) |

| 358 | Y | COX | COM | Rapeseed-EURONEXT(MATIF) |

| 397 | N | FO | FOX | FOX Index-HEX |

| 406 | Y | KLI | FKL | KLSE Comp Index-MDEX |

| 424 | N | EV | EV9 | Electricity-Palo Verde-NYMEX |

| 425 | N | YW | YWH | Wheat-SFE |

| 432 | Y | NP9 | NP | Henry Hub Natural Gas Penultimate-NYMEX |

| 434 | N | WH | WHE | Wheat-EOE |

| 436 | N | BL | BLE | Wheat-Milling-(MATIF)-EURONEXT |

| 449 | Y | SP10 | SP0 | S&P 500 Index (Divided by 10) -CME |

| 467 | N | GL | GLD | JSE All Gold Index-SAFEX |

| 495 | N | YV | YVE | Electricity-Victoria-SFE |

| 516 | N | JD | JDT | Cocoons-Dried-CCX |

| 535 | N | ME | MFT | Govt Bond-Spanish 30 Yr-MEFF |

| 547 | N | FL | FLI | Euro LIBOR-3 Mth-EUREX |

| 555 | N | EB | EBJ | Euro German Pfand |

| 571 | N | OC | OCU | Euro LIBOR-3 M-EURONEXT(LIFFE) |

| 574 | N | OS | OSS | Sterling Rate-3 Mth-EURONEXT(LIFFE) |

| 593 | N | DE | DE2 | Dow Jones Composite Average-CBT |

| 614 | Y | YBA2 | YB2 | 90 Day Australian Bank Bills -SFE |

| 615 | Y | YTT2 | YT2 | 3-Year Australian Govt Bond (6%) -SFE |

| 616 | Y | YTC2 | YT3 | 10-Year Australian Govt Bond (6%) -SFE |

| 631 | N | YB | YBR | Barley-SFE |

| 632 | N | YC | YCN | Rapeseed(Canola)-SFE |

| 648 | Y | SSI2 | SS2 | Nikkei 225 Index -SGX(SIMEX) |

| 664 | N | JP | JPO | Potatoes-YCE |

| 665 | N | JS | JST | S&P/Topix 150 Index-TSE |

| 687 | N | EG | EGT | Sunflower Seeds-EURONEXT(MATIF) |

| 705 | Y | F0B | FBM | Phelix Electricity Base Load-EEX |

| 706 | Y | F0P | FPM | Phelix Electricity Peak Load-EEX |

| 707 | Y | F0C | FBQ | Phelix Electricity Base Load Qtr-EEX |

| 708 | Y | F0Q | FPQ | Phelix Electricity Peak Load Qtr-EEX |

| 709 | Y | F0D | FBY | Phelix Electricity Base Load Year-EEX |

| 710 | Y | F0R | FPY | Phelix Electricity Peak Load Year-EEX |

| 728 | Y | YAP2 | YA2 | SPI 200 Index -SFE |

| 885 | Y | SP1 | SP3 | S&P 500 Index-CME |

| 888 | N | RL1 | RL2 | Russell 2000 Index -CME |

| 905 | N | TM | TMI | Dow Jones Total Market Index-CBT |

| 971 | N | FA | FAP | Potatoes-EURONEXT(LIFFE) |

| 977 | N | TT | TTB | T-bills (91 Day)-TDE |

| 983 | Y | WSA | WEA | Wheat-SAFEX |

| 1056 | N | AXJ | AXJO | mini S&P/ASX 200 Index-ASX |

| 1093 | N | WEI | WWR | Wheat-RMX |

| 1102 | Y | GOC | QOC | miNY Gold-COMEX |

| 1630 | Y | DJ0 | DJO | DJS 600 Food & Beverage-EUREX |

| 1631 | Y | DE0 | DEO | DJ Stoxx Food & Beverage-EUREX |

| 1651 | Y | RS0 | RSO | Refined Soy Oil-NCDEX |

| 1854 | Y | EDL | IED | Eurodollar |

Option Strike Changes for UA

Option strikes now have an extra 1/2 tick for the following markets:

| CSI # | Symbol | Market |

|---|---|---|

| 44 | US | US T-Bond |

| 74 | FF | 30 Day Federal Funds |

| 150 | TY | 10 Tear US T-Note |

| 251 | FV | 5 Year US T-Note |

| 382 | TU | 2 Year US T-Note |

| 1507 | UL2 | Ultra T-Bond |

| 1910 | UT1 | Ultra Bond Week 1 |

| 1911 | UT2 | Ultra Bond Week 2 |

| 1912 | UT3 | Ultra Bond Week 3 |

| 1913 | UT4 | Ultra Bond Week 4 |

| 1914 | UT5 | Ultra Bond Week 5 |

| 1915 | CG1 | 30 Year T-Bond Week 1 |

| 1916 | CG2 | 30 Year T-Bond Week 2 |

| 1917 | CG3 | 30 Year T-Bond Week 3 |

| 1918 | CG4 | 30 Year T-Bond Week 4 |

| 1919 | CG5 | 30 Year T-Bond Week 5 |

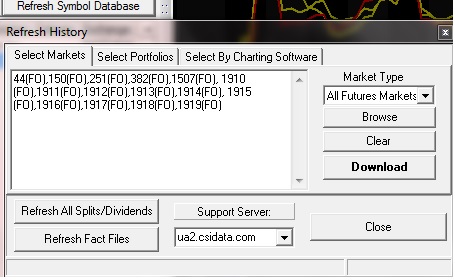

You will need to refresh your databases.

To refresh, click the Refresh Symbol Database button, and then Copy/Paste the following text into the Select Market tab box:

44(FO),74(FO),150(FO),251(FO),382(FO),1507(FO),

1910(FO),1911(FO),1912(FO),1913(FO),1914(FO),

1915(FO),1916(FO),1917(FO),1918(FO),1919(FO)

(Exclude those you are not interested in)

Then click Download. ( Refer to image below for guidance )

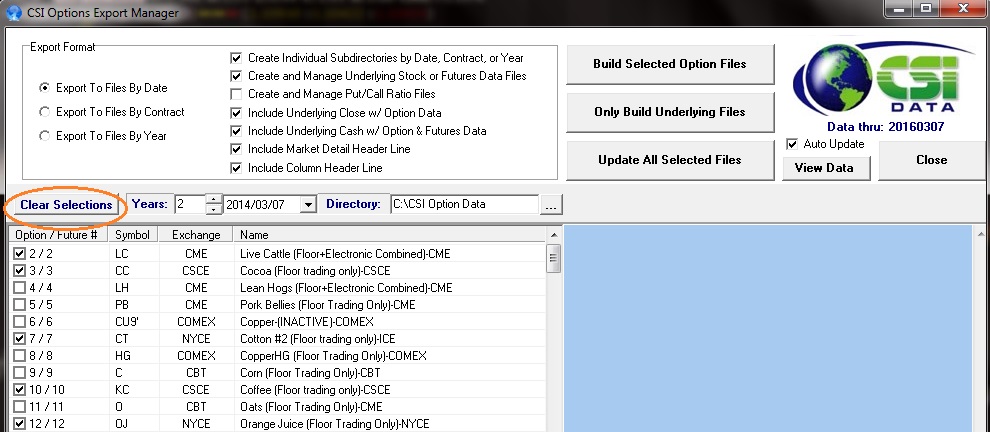

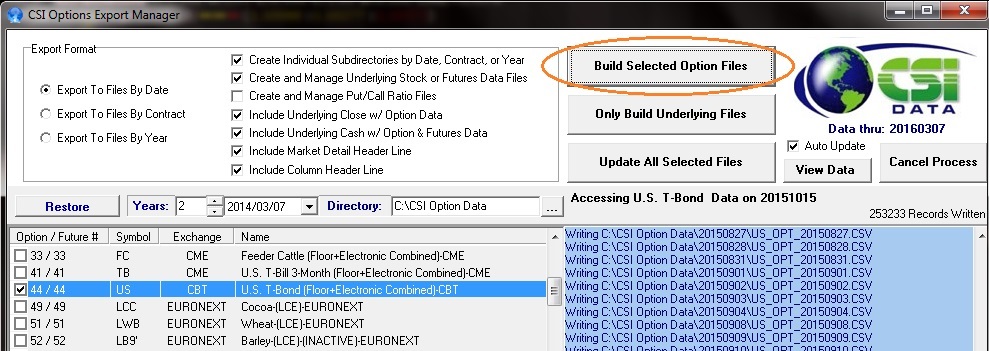

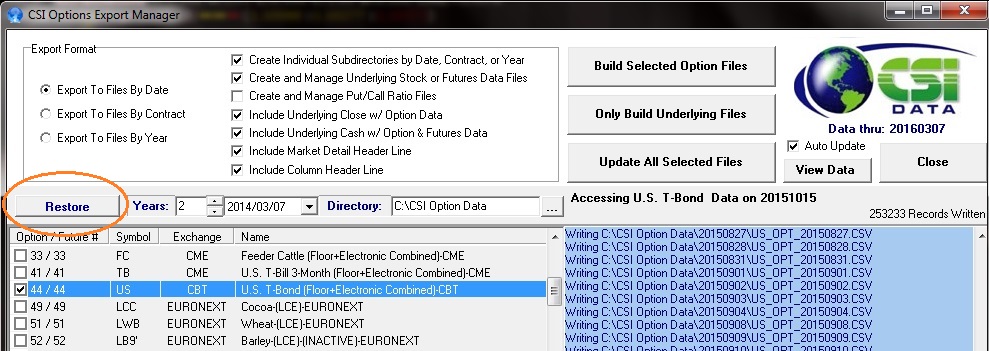

If you’re using the Portfolio Manager to manage your options, you will have to delete all your strikes and re-enter them. I would recommend that instead of re-entering them, that you use the new options export utility which is much more user friendly and much less time consuming.

From within the Export Options Data tool ( Ctrl-O ):

- Click the Clear Selections button to temporarily clear the list of option markets that you’re tracking

- Check ALL the items from the above table that you’re interested in tracking

- Click the Build Selected Option Files button

- When this process has completed, click the Restore button to reselect your markets

- Keep your files updated with the Auto Update feature

( Refer to image below for guidance )

EURO FX MINIMUM TICK CHANGE — 2016 JANUARY 6

Effective Sunday, January 10, 2016 for trade date Monday, January 11, 2016 the Chicago Mercantile Exchange will amend the minimum price increment for Euro FX Futures. The minimum tick is changing from 0.0001 to 0.00005.

UA users will need to refresh the database history for the affected data sets.

Click here for instructions.

CSI issues affected:

#524 CU

#454 CU2

#876 CU1

#499 EX

#100415 M6E

MSCI SINGAPORE INDEX MINIMUM TICK CHANGE — 2015 Oct 29

Effective Monday, November 2, 2015, the Singapore Exchange will change the tick size for MSCI Singapore Stock Index futures and options. The minimum tick is changing from 0.1 to 0.05. Additionally, the contract multiplier will change from S$200 to S$100. All open positions will be doubled.

UA users will need to refresh the database history for the affected data sets.

Click here for instructions.

CSI issues affected:

#539 SSG

#100168 SS4

#100169 SS3

CME Group Closes Most Open Outcry Futures Trading in Chicago and New York July 6 — 2015 June 30

The CME Group has closed all pit futures trading as of July 6, 2015 with the exception of the S&P 500 Index futures. Pit trading of options on futures contracts will remain open.

CSI will continue to report values for the data sets that represent pit-only trading. There will be only settlement pricing, as well as volumes and open interest.

The volumes will consist of Privately Negotiated Transactions (Exchange Futures for Physicals, Exchange Futures for Risks, Exchange Futures for Swaps), plus open outcry volume related to options trading (futures/options combo orders a.k.a. covered spreads, which are a unique delta-neutral instrument created by combining an outright option or options spread with one or more underlying outright futures instruments. The futures leg of such orders is still allowed to be executed via open outcry provided the whole order is executed simultaneously at the spread’s differential price. These orders are executed in the open outcry options pits, which are still open.)

The following table lists the various markets affected, with CSI numbers for the electronic trading (ETH), pit trading (RTH), and combined market data:

| Pit/RTH | Globex/ETH | Combined | |

| Agricultural | |||

| 18 | 894 | 410 | soymeal |

| 19 | 895 | 411 | soyoil |

| 9 | 896 | 412 | corn |

| 21 | 897 | 413 | wheat |

| 11 | 898 | 414 | oats |

| 130 | 899 | 415 | rough rice |

| 110 | 100189 | 100190 | mini wheat |

| 111 | 100191 | 100192 | mini corn |

| 112 | 100193 | 100194 | mini soybeans |

| 694 | 886 | 2 | live cattle |

| 695 | 887 | 4 | lean hogs |

| 696 | 889 | 33 | feeder cattle |

| 100364 | 100365 | 27 | lumber |

| 100227 | 100228 | 404 | class 3 milk |

| 22 | 100067 | 100666 | kc wheat |

| Currency/FX | |||

| 278 | 875 | 23 | mexican peso |

| 127 | 878 | 25 | swiss frac |

| 128 | 879 | 26 | british pound |

| 129 | 880 | 64 | canadian dollar |

| 262 | 877 | 65 | japanese yen |

| 265 | 884 | 66 | australian dollar |

| 454 | 876 | 524 | euro |

| 458 | 100061 | 100060 | south african rand |

| 459 | 100063 | 100062 | new zealand dollar |

| 100568 | 100555 | 100569 | fx index |

| 519 | 100065 | 100064 | russian ruble |

| Financial | |||

| 269 | 881 | 141 | eurodollar |

| 270 | 883 | 142 | libor |

| 144 | 801 | 44 | 30 yr tbonds |

| 250 | 802 | 150 | 10 yr note |

| 293 | 803 | 251 | 5 yr note |

| 666 | 804 | 382/207 | 2 yr note |

| 750 | 892 | 74 | fed funds |

| 100506 | 100508 | 100507 | ultra t bonds |

| 100136 | 100137 | 416 | euroyen |

| 100835 | 100834 | 100833 | 30yr interest rate swap |

| 100838 | 100837 | 100836 | 10yr interest rate swap |

| 100841 | 100840 | 100839 | 5yr interest rate swap |

| 100844 | 100843 | 100842 | 2yr interest rate swap |

| Equity index | |||

| 912 | 831 | 99 | nikkei US |

| 688 | 100406 | 266 | goldman sachs index |

| Metals | |||

| 8 | 864 | 809 | copper |

| 16 | 863 | 868 | silver |

| 30 | 862 | 867 | gold |

| Energy | |||

| 13 | 379 | 859 | platinum |

| 69 | 810 | 849 | palladium |

| 89 | 377 | 857 | heating oil/ny harbor |

| 188 | 376 | 856 | crude oil |

| 191 | 860 | 869 | natural gas |

| 975 | 866 | 976 | rbob gasoline |

*CSI numbers >100,000 are denoted in UA as >1,000. e.g. CSI# 100406 is UA# 1406

Japanese Yen minimum tick change — 2015 June 15

Effective Sunday, June 21, 2015 for trade date Monday, June 22, 2015 the Chicago Mercantile Exchange will amend the minimum price increment for Japanese Yen/US Dollar Futures. The minimum tick is changing from 0.000001 to 0.0000005.

UA users will need to refresh the database history for the affected data sets.

Click here for instructions.

CSI issues affected:

#65 JY

#262 JY2

#877 JY1

#498 JT

#1817 MJY